Update from March 4, 2020:

We won!

__________________

Original post on November 22, 2019:

I live in a town across the Golden Gate Bridge called Mill Valley. My wife and I moved here in 1999 with our two small children who were 4 and 1 years old at the time. It was near the end of the dot.com bubble. We were both consultants living in Silicon Valley and experienced this period up close.

I told my wife that I thought we were buying our house at the top of the market. She turned to me and said: "We are not buying a house, we are buying a home. This is where we raise our children. This is where we make our life."

As usual, she was right. I coached Little League and soccer for 10 years. My kids both ran the Dipsea Race every year. My son became an Eagle Scout. We all volunteered for our local library. Both kids started kindergarten here and graduated from the local high school, all public. They've now moved away. They're adults.

Outside of work and writing The Fat Pitch, I have run a 501(c) benefiting our library and chaired our town's Planning Commission. We love this town, we want to make it the best it can be, we will never leave. We believe in action, not words. We don't just talk, we do.

In September, I wrote a piece on the US economy and then went on a trip overseas for the rest of the month. When I returned, I started a campaign to run for elected office on our town's City Council. I met with every living former mayor, explained who I was and what I wanted to accomplish, and was endorsed by all, 19 in total. I am doing the same with as many other community leaders as I can and if they are in a position to endorse a candidate, then they have endorsed me. I am extremely grateful and humbled by everyone's support and encouragement. This feels right. I'm excited.

This has been time consuming, but I can't think of anything more important. I sat with an owner of a vital and iconic shop in downtown Mill Valley this week, a person raised here, retired here and who has over the past several decades met with every future mayor. He grilled me on housing, finances, traffic, human resources and every other topic of importance. 90 minutes went by like it was 5. It was thrilling, and I once again learned many things I didn't know the day before.

I have never run for public office. I never thought this is where life would lead me. I'm 56 years old, I have lived here for 20 years, I have been deeply involved in my community and I feel like I can make a difference. I don't have an answer for everything, there's a lot I don't know, but I will listen, I will ask questions, I will study, I will act with integrity and honesty, I will give this my every effort and I will try to do the right thing.

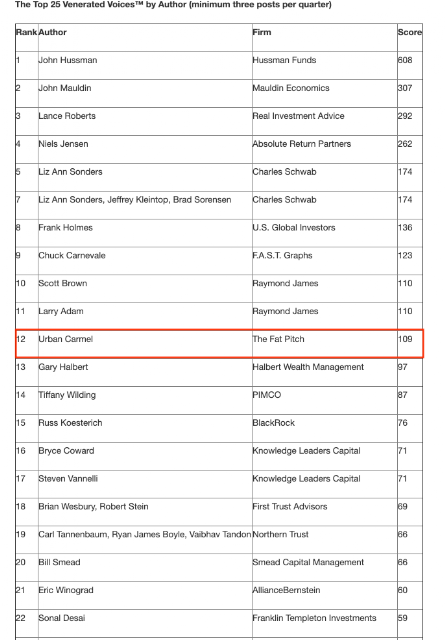

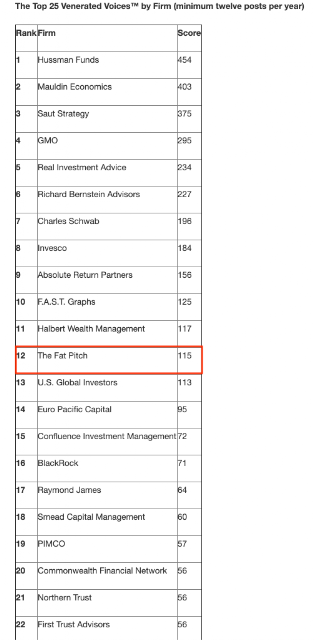

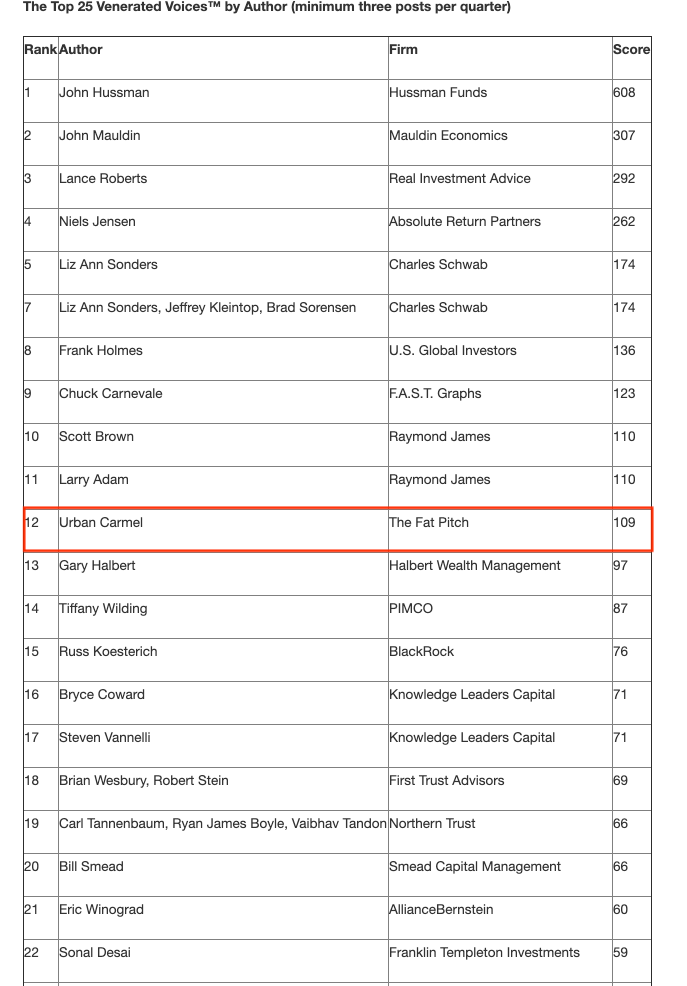

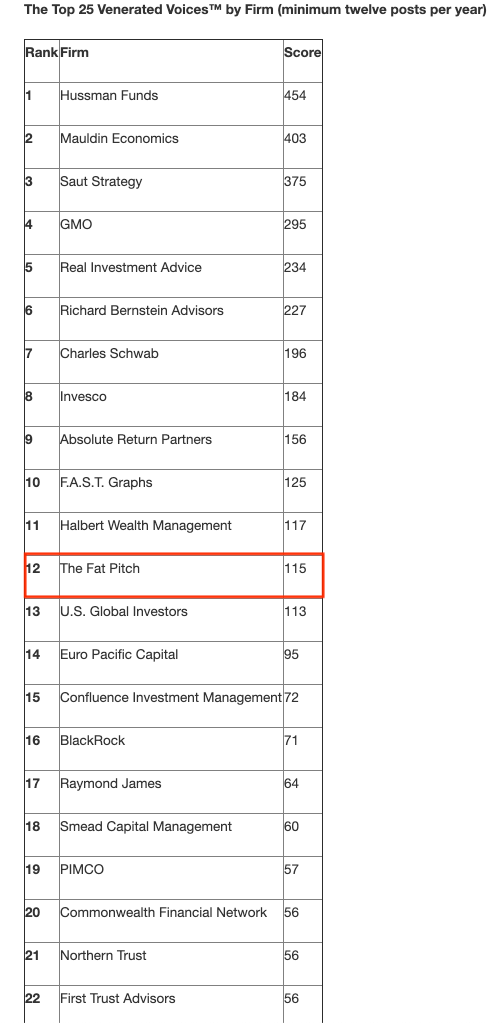

I have put a lot of effort into writing The Fat Pitch. I have wanted it to be the best source of financial and economic analysis that I could create. I wanted to help anyone willing to read it to learn and question and think and hopefully improve. It did all of those things for me. I don't believe in half measures, so I haven't written in a while. When I can commit the needed time, I will start writing again. I miss it, I'm committed to it and I will return to it.

If you are reading this and happen to live in Mill Valley, please get in touch. If you know someone here, spread the word. I am trying to run a different type of campaign, one where thousands of mailers and hundreds of lawn signs are replaced by email, phone calls, meetings at coffee shops and by my feet walking in neighborhoods. I want every voter to have met me, read about me or to have heard about me from a trusted friend. I don't want a vote based on a lawn sign or a piece of mail. That is all landfill. The recent fires and power shutdown in California are a timely reminder that we need to change the way we do things, and it starts with something as simple as a local election. It starts now.

You can read more here:

https://urbancarmel.com/